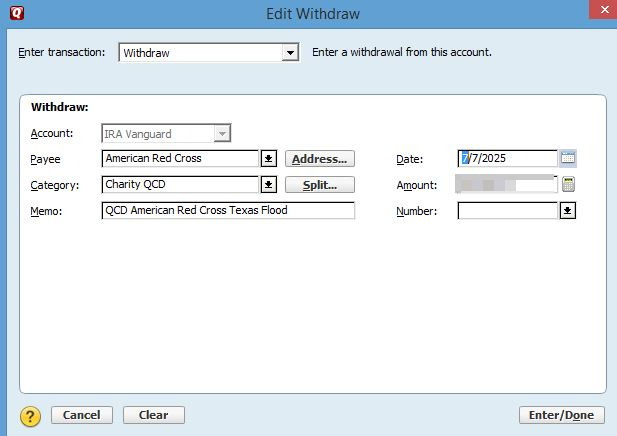

If this has already been asked and answered, I apologize. I didn't see any recent posts. The issue of taking an RMD and showing the taxable transfer has been fixed. These show as "WithdrwX" in the register and works great. This year, I made a couple of QCD's. I'm not sure how to show them. I tried doing just a withdraw. It shows as "Withdrw" in the register. This did not show on the tax planner as taxable income. I tried writing a check in the IRA account. It shows as "Writechk" in the register. Again, this did not show on the tax planner as taxable income. The IRA account does show Transfer Out as "1099-R Total IRA Taxable Distribution". Do I need to go back and 1st withdraw and transfer the money to a dummy account?

Thank You

Mike