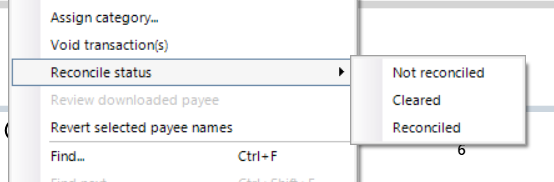

I have one credit card account where transactions within the last day or two of the end of the billing cycle don't show up on the next bill even though their posting date is within the date range for the bill. When I reconcile the bill in Quicken, I have to un-check those cleared (downloaded) transactions to get the bill to balance. That's fine. What annoys me is that doing this marks the transactions in the register as uncleared, so I have to go through them all again and re-mark them as cleared. Unchecking a cleared transaction in the bill reconciliation window should just leave that transaction as cleared but not reconciled.