How to set up a fixed income annuity

How can I set up a fixed income annuity. I'm basically taking some money from an IRA, let's say $100,000 and it pays me a guaranteed annual income for the rest of my life, let's say $10,000/yr. If I pass before the $100,000 is used up, it goes to my beneficiaries. But after 10 years, I continue to get $10,000/yr for the rest of my life

So for the first 10 years, it still has some value. After 10 years, the money just continues to come.

The annuity doesn't vary in value, so shouldn't be any need to download current prices or anything like that.

Best Answer

-

The annuity is still in the IRA, right, so there is no tax when you set it up and you pay tax as income on the distributions.

Quicken does not have a special account type for annuities, but you could set up an offline IRA account or an Asset account and transfer the $100k to that. If you want to exclude the death benefit from your Net Worth and other reports, you can mark the account as Separate. Then track the distributions like other IRA distributions, as follows:

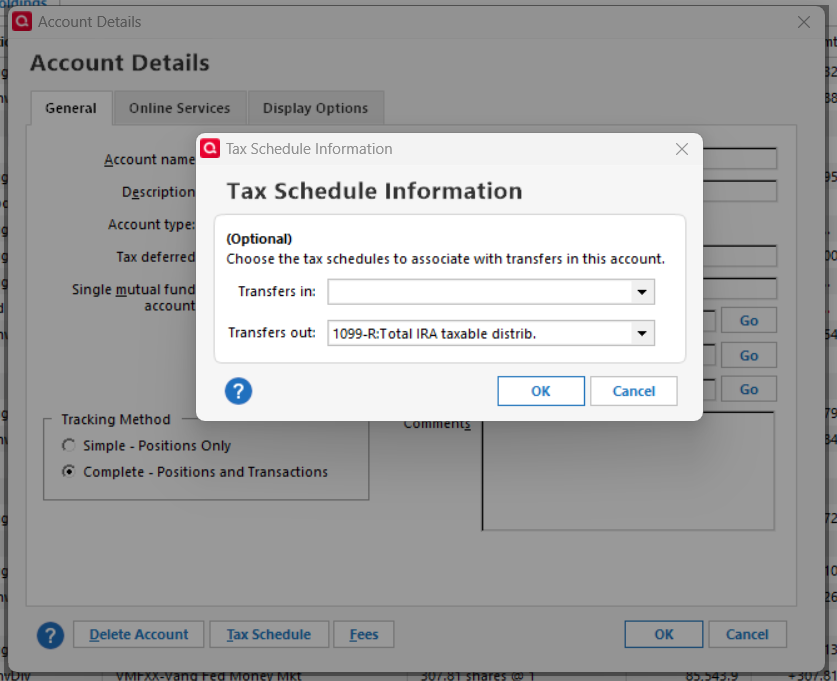

In the new account, click on the gear at the top right and select Edit account details. Click on Tax Schedule and set Transfers out to the appropriate tax line item, which might be 1099R: Total IRA taxable distrib. or 1099-R:Total Pension taxable distrib., like this:

For the taxes to be recorded properly in Quicken, the transfer must be entered as a Deposit transaction in the receiving account. It can be a banking or an investing account, but it must be a taxable account, not another IRA for example. If there is already an Xout transaction in the IRA account that transfers money to the taxable account, note the amount and delete it before entering the Deposit. Do not try to edit the receiving end of the transfer.

In the receiving account:

1) Enter a Deposit transaction for the net amount of the distribution...a positive number.

2) Split the category:

- Line 1 of the split: Category = the IRA account name in [square brackets] and the gross distribution amount...a positive number.

- Line 2 of the split: Category = the Fed taxes withholding category that you use...a negative number.

- Line 3 of the split: Category = the State taxes category that you use...a negative number.

- Total of the split: Must equal the net amount of the deposit.

If you receive the distributions regularly, you can set this transaction up as an Income Reminder.

In the annuity account: Delete any downloaded brokerage transactions for

- The net distribution

- The Fed taxes withheld

- The State taxes withheld

With this setup, the taxable income will be shown in the “1099-R Total IRA Taxable distrib.” and the tax withholding in the withholding sections of the Tax Schedule report.

As the death benefit declines, you could click on the gear in the account and select Update cash balance to reset the balance.

For more information on tracking annuities in Quicken, see this discussion

QWin Premier subscription1

Answers

-

"So for the first 10 years, it still has some value. After 10 years, the money just continues to come."

So it still has value, even after 10 years, if you live that long.

Does the annuity earn interest along the way? You'd probably want to make entries for any interest earned as it accrues.

Accounting for an individual annuity with screaming accuracy is near-nigh impossible. Companies that issue these things, and have to show Liabilities on their balance sheets, (the reverse of you showing an asset on yours), can themselves only make estimates based on assumptions of longevity and using the Law of Large Numbers to make these estimates "reasonable."

I'd probably suggest taking the easy way out and simply entering interest as earned, deducting the payouts against the Account's balance, and recording any money received after that just as a form of income.

1 -

The annuity is still in the IRA, right, so there is no tax when you set it up and you pay tax as income on the distributions.

Quicken does not have a special account type for annuities, but you could set up an offline IRA account or an Asset account and transfer the $100k to that. If you want to exclude the death benefit from your Net Worth and other reports, you can mark the account as Separate. Then track the distributions like other IRA distributions, as follows:

In the new account, click on the gear at the top right and select Edit account details. Click on Tax Schedule and set Transfers out to the appropriate tax line item, which might be 1099R: Total IRA taxable distrib. or 1099-R:Total Pension taxable distrib., like this:

For the taxes to be recorded properly in Quicken, the transfer must be entered as a Deposit transaction in the receiving account. It can be a banking or an investing account, but it must be a taxable account, not another IRA for example. If there is already an Xout transaction in the IRA account that transfers money to the taxable account, note the amount and delete it before entering the Deposit. Do not try to edit the receiving end of the transfer.

In the receiving account:

1) Enter a Deposit transaction for the net amount of the distribution...a positive number.

2) Split the category:

- Line 1 of the split: Category = the IRA account name in [square brackets] and the gross distribution amount...a positive number.

- Line 2 of the split: Category = the Fed taxes withholding category that you use...a negative number.

- Line 3 of the split: Category = the State taxes category that you use...a negative number.

- Total of the split: Must equal the net amount of the deposit.

If you receive the distributions regularly, you can set this transaction up as an Income Reminder.

In the annuity account: Delete any downloaded brokerage transactions for

- The net distribution

- The Fed taxes withheld

- The State taxes withheld

With this setup, the taxable income will be shown in the “1099-R Total IRA Taxable distrib.” and the tax withholding in the withholding sections of the Tax Schedule report.

As the death benefit declines, you could click on the gear in the account and select Update cash balance to reset the balance.

For more information on tracking annuities in Quicken, see this discussion

QWin Premier subscription1 -

»Does the annuity earn interest along the way? You'd probably want to make entries for any interest earned as it accrues.

No interest. The insurance company takes on the risk of interest fluctuations. So I just get a fixed amount, no matter what

»The annuity is still in the IRA, right, so there is no tax when you set it up and you pay tax as income on the distributions.

I wouldn't describe it like that. More like I took money and transferred it to another IRA account. But yes, all distributions are taxable.

Why do you say that the original transfers should be a taxable account and not another IRA? Are you talking about for each distribution? Wouldn't the cash balance decrease automatically this way? What do I do when the cash balance goes to 0 and the money keeps coming in?

0 -

The distributions should be made to a taxable account so that they will be picked up by the Tax reports.

Yes, the distributions will reduce the cash balance, and the death benefit will also go down over time but probably not by the same amount. Because transactions inside the account are not taxed, you don't have to keep track of income or capital gains, you can just adjust the cash balance to match the amount of the death benefit.

QWin Premier subscription1 -

There are no transactions inside the annuity except for the distributions so very easy to keep track of

0 -

While the distributions are all 100% taxable because they are from an IRA, you may want to track the value of the annuity for estate net worth purposes. The day you buy it is worth $100K, but with every distribution you are receiving a combination of principal returned and interest earned. The value of the annuity for estate net worth decreases by the principal amount of each distribution.

The annuity company should have provided a schedule of principal and interest payments for the life of annuity. That schedule will be longer than 10 years as principal payments and interest payments are scheduled over your calculated life expectancy. Stated simply, your annuity will still have value after 10 years as the principal will be distributed over your lifetime. The 10 years is just a guarantee that you or your beneficiary will get a $100K back. The annuity company keeps all the earnings from the $100K amortized over 10 years. They don't start losing money (paying out the full $10K) until after your actuarial life expectancy.

1

Categories

- All Categories

- 22 Product Ideas

- 34 Announcements

- 247 Alerts, Online Banking & Known Product Issues

- 19 Product Alerts

- 518 Welcome to the Community!

- 682 Before you Buy

- 1.5K Product Ideas

- 55.7K Quicken Classic for Windows

- 16.9K Quicken Classic for Mac

- 1K Quicken Mobile

- 834 Quicken on the Web

- 128 Quicken LifeHub