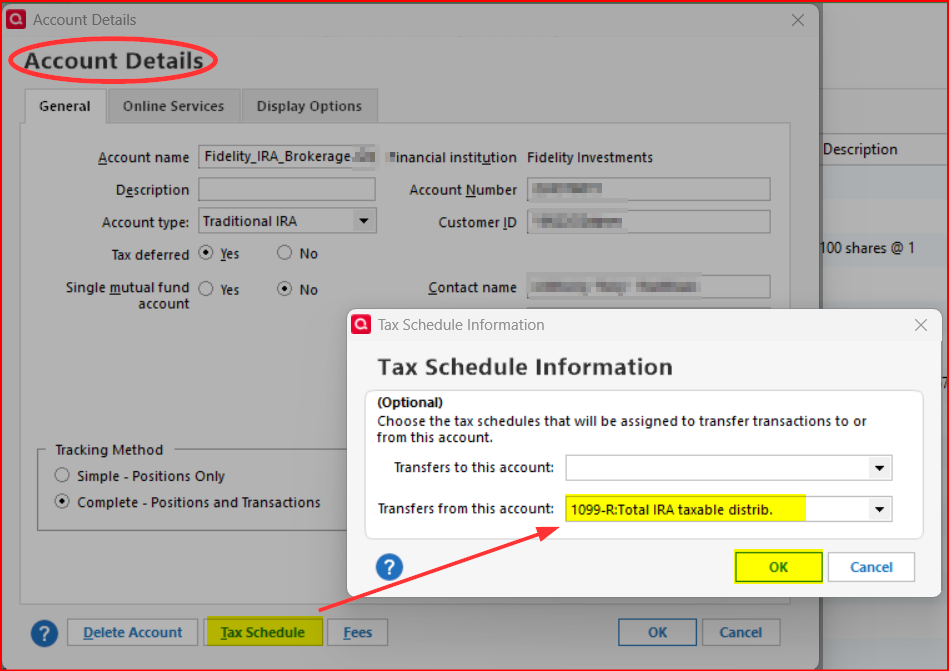

Using Quicken Classic Premier. Account type is Traditional IRA.

Trying to remove money from the account and have the RMD withdraw appear in my Tax Planner. I can't seem to get this to work.

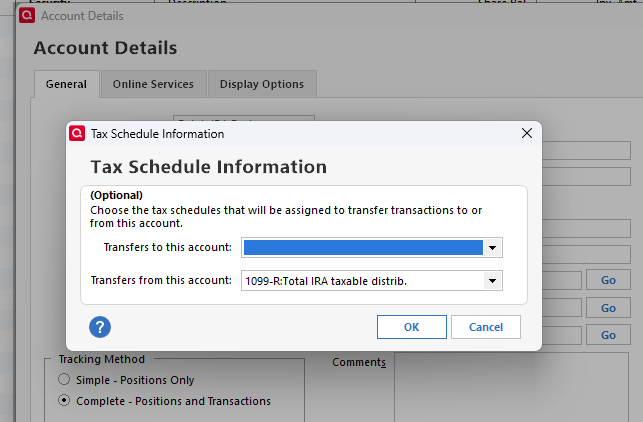

I made a new category and labeled it RMD. I set it as Income. Set it as tax reporting 1099-R Total IRA taxable distribution.

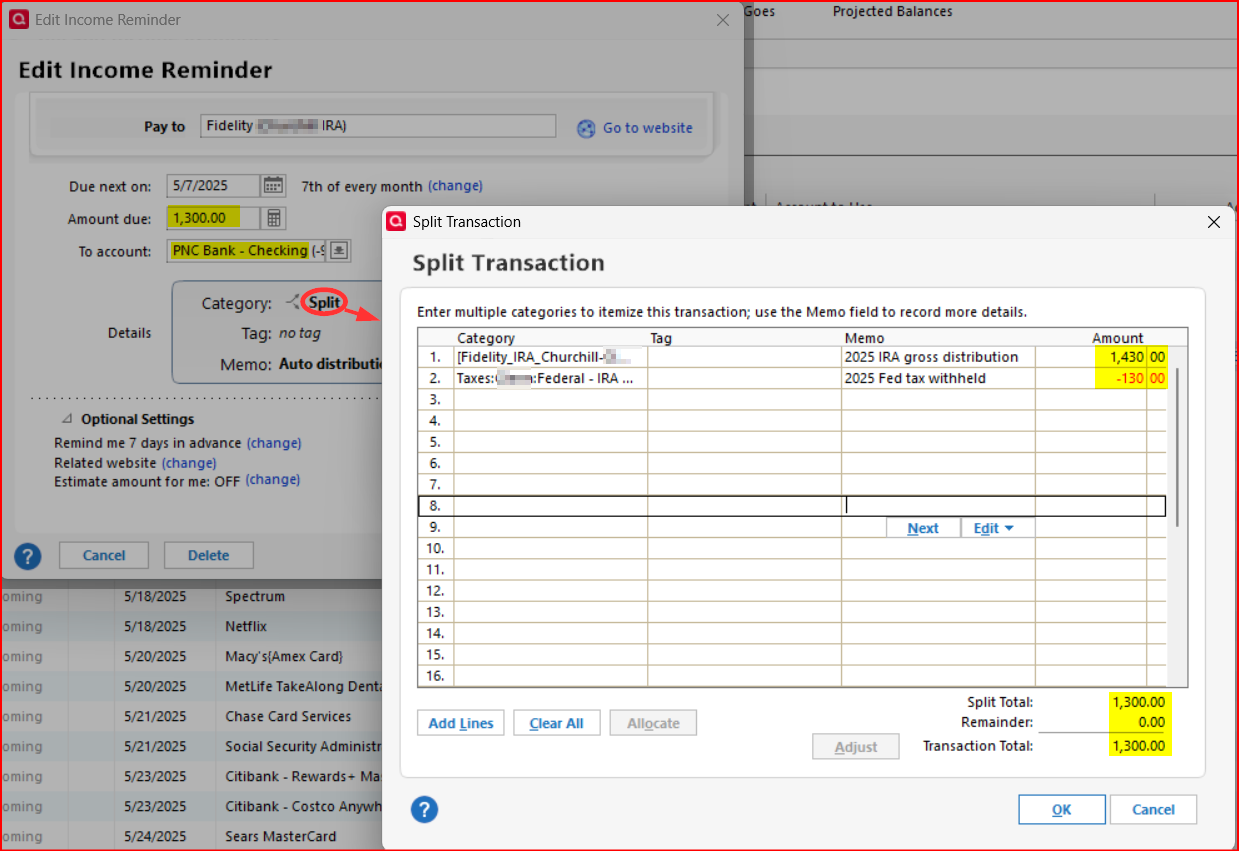

I added a new line to the IRA account as a 'withdrawl' and set the category to RMD. It doesn't apprear in the Tax Planner.

Can someone please tell me what I am doing wrong? And possibly how to fix this? thank you.