hi,

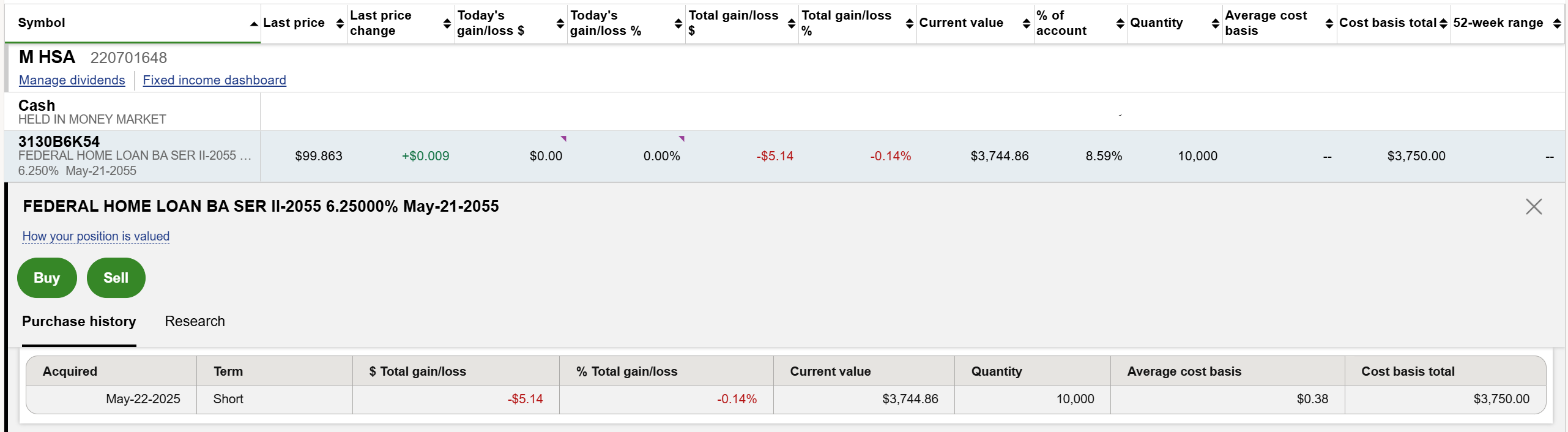

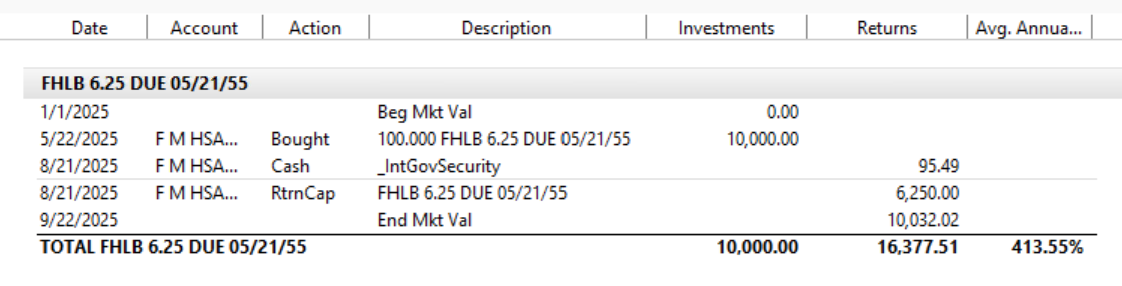

My Gov Agency Bond was partially called.

I bought 10000 for $10,000.00

The $6250.00 was called and I got back this as Principal. My cash position in my Fidelity account was increased by $6250.00.

The $3750.00 remains for this Bond / CUSIP.

How to record this partial call correctly in the Quicken?

There are my current issues:

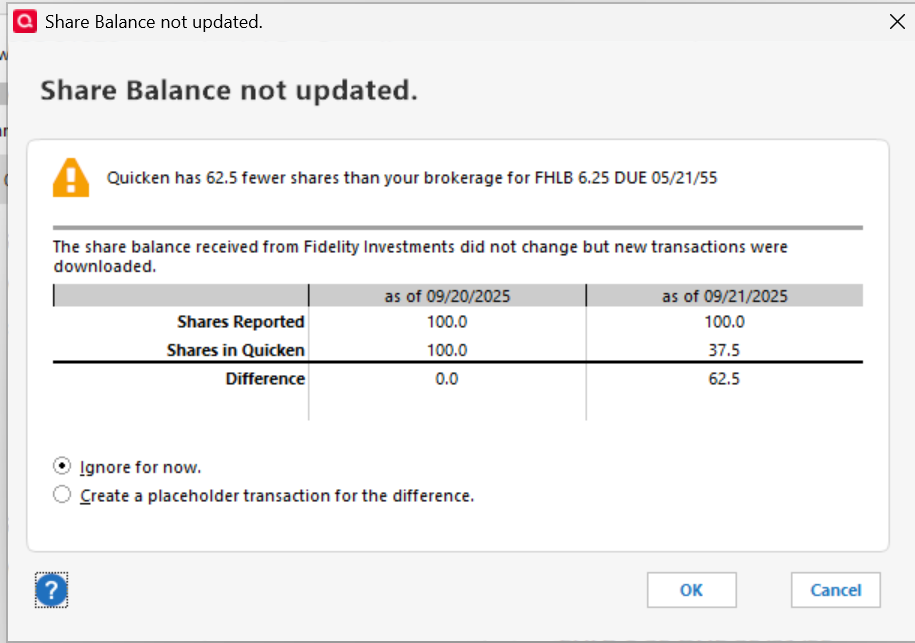

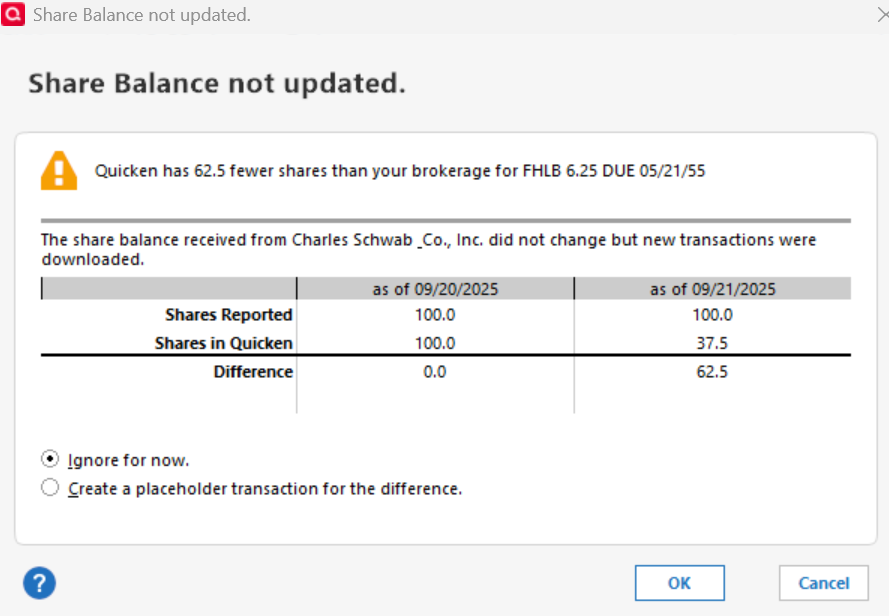

- The Fidelity, as well as Schwab all reports the same original number of shares as 10,000.00, if I record this as 6250 bonds Sale then I have Securities mismatch

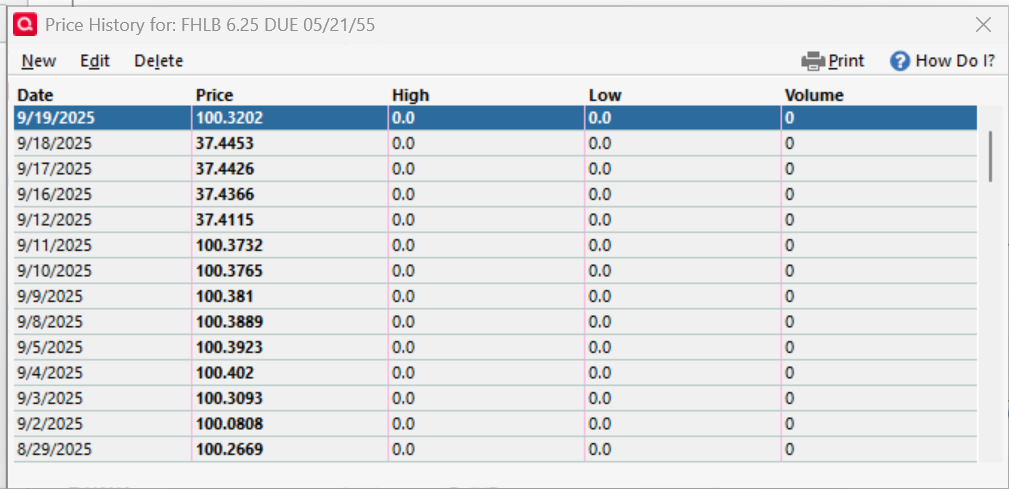

- The Fidelity, as well as Schwab all reports new share price as just $0.375, instead of original $1.00/share. This leads to incorrect performance related calculations, it shows 62.5% Losses, while there are none.

This is 1st time for me such partial Bond call of the principal.

How to properly record this?

Yes, I called Fidelity and Schwab, both Fixed Income specialists responded this is how it works on Fixed Income side, when the share price gets lowered, while number of shares remains the same. They (Fixed Income) don't track performance in Stock traditional way.

tnx